Some weeks ago, at CFTE we started our “One Fintech chart a day” series in an attempt to bring granular but constant awareness about the rising importance of platform business models in finance. A number of metrics have been explored since to show the dramatic rise of this model in financial services and a number of key findings have emerged. This article will explore some of the key themes of our first 3 weeks of findings.

The top 3 financial platforms have recorded a collective growth of over 800%, much similar to Big Techs than FIs

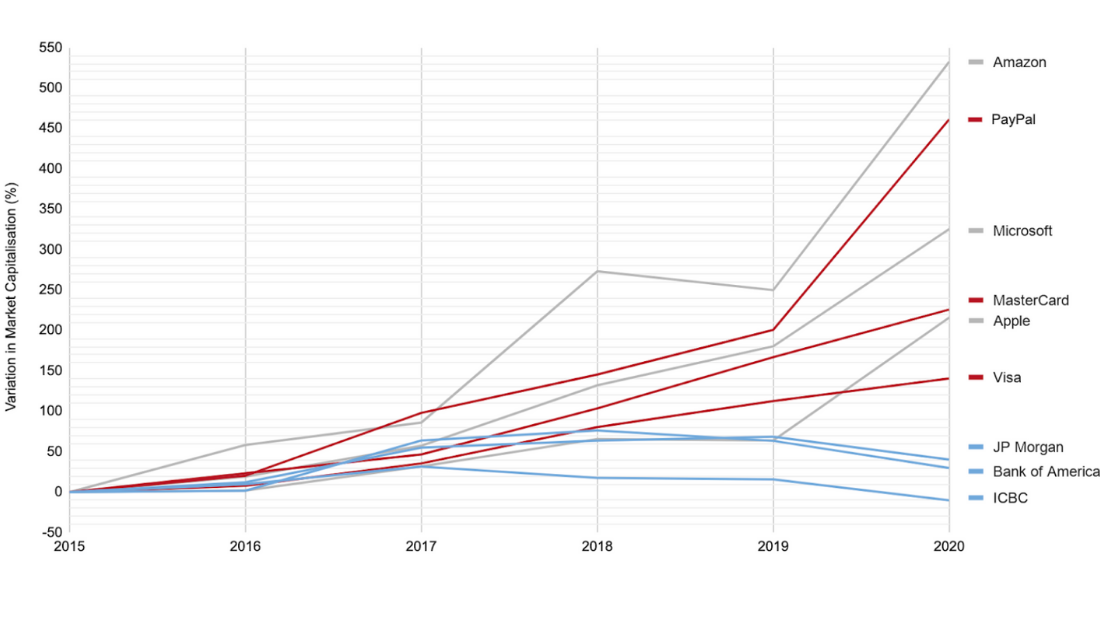

Since 2015, the growth of traditional financial institutions has been stagnant, with the top 3 global banks – JP Morgan, Bank of America and ICBC – recording a collective growth of only 60%. By comparison, during the same period the top 3 financial platforms – MasterCard, Visa and Paypal – have recorded a collective growth of over 800%. The largest financial institutions are now dominated by platform-based companies.

The growth of these financial platforms is impressive and, in fact, is not far off the seemingly untouchable growth experienced by the US big tech giants, the supposed jewel in the global economy. Amazon, Apple and Microsoft have achieved a collective growth of around 1074% since 2015. While these financial platforms may still be a long way off the valuations of Big Tech, their aggressive growth is dramatic.

It must be noted that our chart in figure X does not consider the Chinese financial platform giants of Ant Group and the fintech arm of Tencent. In fact, if Ant Groups IPO had not been halted in early November, it’s growth of 596% since 2015 would have been 4 times greater than growth of the top 5 global banks combined and greater than any US tech giant during this period.

The fundamental differences in the markets that these three segments operate in limits the descriptive power of our findings. However, what is clear is the landscape of financial services is changing and, so far, the pioneers of this change are all leveraging the platform model to facilitate growth that even the tech titans in Silicon Valley may be proud, or even, jealous of.

The rise of the platform model

While we do not claim causality between the adoption of the platform model and the aggressive growth of platform-based financial institutions, the correlation is interesting.

The last 10 years have brought around dramatic changes in market conditions, and it appears that a number of companies are adopting the platform model to capitalise on technological advancements and create new and exciting products to fulfill the ever increasing expectations from consumers. This trend is now quite clearly entering financial services, and traditional banks need to take note.

Stagnant banks

The stagnant growth of traditional banks is driven in part by net interest margin squeezes, increased competition and substantial compliance and infrastructure costs. It suggests banks need to re-evaluate their model to capitalise on technological trends, meet the growing demands of consumers and explore new value propositions. The platform model may be the key to facilitate this change.

The adoption of the platform model combined with modern, cloud based and API-driven banking software, as well as a clear strategy for partnerships with the new financial ecosystems, may allow traditional financial institutions to diversity their value propositions and develop a range of new and exciting products for increasingly demanding consumers.

While the adoption of the platform model presents a range of extensive challenges for financial institutions, our findings suggest there may be a huge financial promise to those who pioneer this adoption.

Interested in learning more about platforms in financial services?

Latest posts:

- The EU AI Act’s August 2026 Milestone: Is Your Workforce AI Literate?

- Global Women in AI Launches Hong Kong Chapter at LEAP East 2026

- Agentic AI in Financial Services: Governance Has to Move From Policy to Operating Model

- AI Governance Is Not the Brake. It Is the Way Forward.

- UK Finance and CFTE Launch New Offering to Build AI Capability Across UK Financial Services