Fintech businesses are successfully piggybacking on practically all financial services that were previously carried out in the traditional manner, from insurance underwriting to credit profiles to account opening. It has introduced and reversed traditional business models in the sector, examining which models have caused a significant shift in the financial industry.

Business Models in Fintech

Since they began to challenge conventional financial service companies, including the traditional banking model, Fintech enterprises have gotten a lot of attention in recent years. In this article, we will examine the main business models in Fintech and the benefits that digital transformation provides to them. Clients, financial institutions, banks, and corporations, among others, have already adopted a number of Fintech business models. Let’s look at the top 10 FinTech business models that are paving the way for innovation disruption:

1. Digital Banking

Consider your standard brick-and-mortar bank going entirely online, with no physical location, bank tellers, or mail. Through a full digital infrastructure, challenger banks like N26 are providing no-frills individual and commercial bank accounts. The business strategy is nearly identical to that of a bank with physical branches, except that consumers can profit considerably from lower rates due to huge cost reductions in people and real estate.

Some banks are beginning to offer personal and business bank accounts through a fully digital infrastructure. This business model is nearly identical to that of a bank with physical branches, with the exception that it does not necessitate high staffing and real estate costs, allowing clients to benefit from lower rates.

2. Digital Wallets (E-wallets)

Electronic wallets are a hybrid of a traditional bank account and a payment processor. Users can preload virtual money into their e-wallets and use it to pay for goods and services using this business model. E-wallets are popular, and since the outbreak, an increasing number of people have begun to use digital payment methods.

Customer benefit convenience as contactless payment made via the internet for a little fee, which is typically charged to businesses in the form of a Merchant Discount Rate (MDR) by Fintech companies. These payment systems also make money by selling their consumers third-party financial services. The cashless future appears to be highly promising, given the ongoing innovation in the development of e-wallet applications. Businesses selling actual products or services to end users in stores, such as Venmo, Square Cash, and others, are typical wallet end users. Global digital payment annual worth has increased 74% over the past six years:

3. Peer-to-peer lending

When an individual borrows money from another individual, this is known as peer-to-peer (P2P) lending. Peer-to-business (P2B) lending, on the other hand, occurs when a company borrows money from one or more individuals. By sending their money to pre-approved and verified borrowers, these lending models make it easier for investors to receive better returns than those available in debt markets. Fintech businesses like Funding Circle build platforms to connect borrowers and lenders, and they typically deduct a charge from the borrower’s repayment.

4. Alternative credit scoring

Due to rigorous and antiquated credit scoring procedures, many self-employed people with a stable source of income fail to pass traditional bank loan screenings. Alternative data elements like social signals and percentile scoring among similar borrower groups are being considered by credit rating Fintech companies like Nova Credit. All of these qualitative characteristics, when combined with a smart, self-learning algorithm, can result in better lending judgments over time. If a lender can identify unfavorable profiles based on social presence prior to loan disbursement, for example, they can avoid dealing with loan recovery.

5. Alternative insurance underwriting

Fintech companies are developing premium computing techniques employing alternative data points such as lifestyle data and medical history, similar to how alternative credit scoring works. Insurance, when combined with AI algorithms, is a powerful tool. Fintech firms can choose whether or not to offer insurance, as well as what terms and conditions to offer and what alternative payment methods to utilize.

6. Transaction delivery

Data is the new oil, and better data management may reveal a wealth of information about a customer’s requirements and desires. Fintech startups in the transaction delivery area are developing free products, such as spending management apps, to collect customer data and then cross-pollinate it with the rest of the group to map the client’s capacity to pay premiums, invest in real estate, buy mutual funds, and so on. Commission-based business models, such as reselling third-party financial products, are used by these types of Fintech enterprises.

7. Payment Gateways

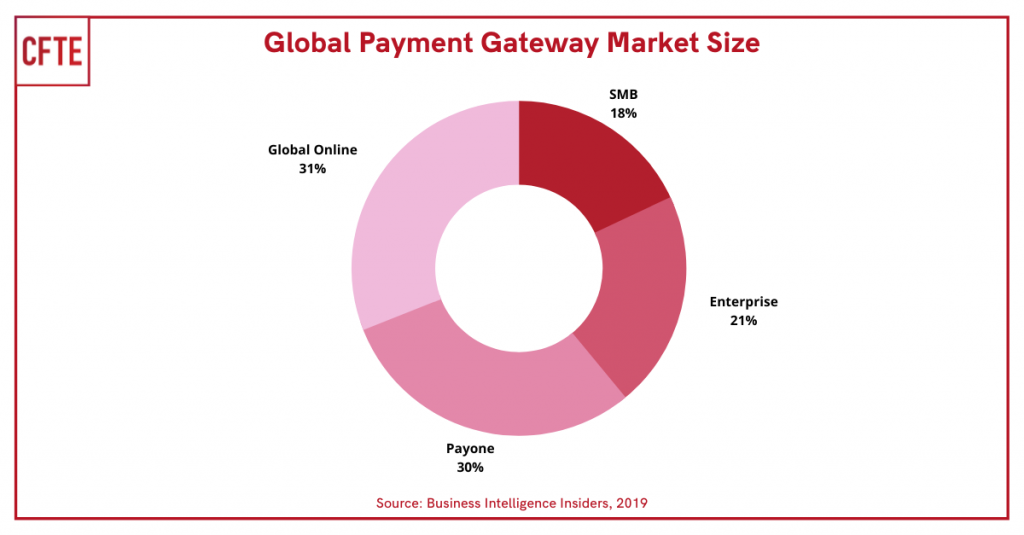

Payment gateways are online payment systems that allow customers to pay for goods and services on a merchant’s website. Debit cards, credit cards, digital wallets, and cryptocurrencies are just a few of the payment options available today. Banks often charge exorbitant fees to handle transactions from all of these different methods, but Fintech startups are merging all of these payment methods into simple apps that internet retailers can easily afford and include on their websites. Businesses selling actual products or services to end customers, such as Stripe, Alipay, and iZettle, are typical users of these payment apps. Below is a pie chart on the global payment gateway based on retail segment composition market size with Global Online taking the lead with 31% followed by Payone 30%:

8. Asset Management

Fintech firms such as Robinhood, are allowing investors to sell for free in exchange for their personal information. They send this information to high-frequency traders with the power to impact the asset’s price. The difference between the amount they save on trading fees and the modest price rise is usually still acceptable.

9. Digital insurance

Fintech companies in the insurance market, are bringing all of the traditional services to the digital realm. These Fintechs’ can price their premiums at variable rates depending on the customer, allowing them to offer aggressively cheaper coverage than traditional insurance firms. They also offer life and health insurance with improved underwriting methods. These sorts of insurance, when combined with tailored marketing, can open up new revenue opportunities for insurance businesses. Lemonade, for example, is in the home insurance industry.

10. Neobanking

Neobanking is a Fintech concept that entails the development of digital platforms – neobanks – that are faster, more efficient, adaptive, and cost-effective. Varied neobanks serve different objectives; some can manage online bank accounts, while others can help with budgeting and saving. There are neobanks that deal with accounting and finance automation, and others that assist with the credit process. According to Business Insiders, Global Neobank Value has accelerated $31.7B more from 2018.

Conclusion

If you are thinking of diving deeper into any of the business models mention above, CFTE is ready to help you to keep up with the latest Financial technologies to gain experience in theoretical and practical fintech knowledge. We have strong knowledge on Fintech trends, innovations, and new business model topics that is led by the best team of professional fintech experts from startups to MNC’s.

Let’s talk about your Fintech opportunities!