What is a Challenger Bank?

- A challenger bank is a new digital bank that has a bank license.

- The most important word is “banking license”: a challenger bank is regulated as a bank

- It is new, so not an existing bank digitalizing its business

- And digital as we mentioned before

Challenger banks, as a result of the advent of Fintech, have been increasing in numbers in recent years. In fact, currently, there are about 100 challenger banks worldwide, offering different types of financial services to a poll of consumers whose banking preferences have shifted towards simpler, more transparent, and digital ways of managing money.

Here’s the list of the top 10 Challenger Banks in 2022 by Market Capitalisation:

1. Nubank

Supported by Tencent and Warren Buffett, NuBank has occupied a substantial position in Latin America, progressing actively from interest-free credit cards to a comprehensive set of financial services.

2. Revolut

Revolut is an aspiring private digital bank, maintaining not only card payments, saving schemes, but an array of services like investments or international transfers.

3. Chime

Chime is a financial services company linked to several banks, which offers a highly user-friendly app with a credit card, savings account and absent fees.

4. WeBank

Brought to life by a consortium of tech companies, WeBank is another private bank, devoted to transparent services and working with underbanked groups.

5. Robinhood

A star of last year’s stock craze, Robinhood is a leading commission-free investment app with a variety of tailored financial instruments, with a set of unique income flows.

6. Tinkoff

Made as an experiment for the Russian market, Tinkoff is the region’s digital banking champion, highlighting openness and big data solutions.

7. Brex

An exemplary Silicon Valley unicorn, Brex occupies the growing niche of banking aspiring tech companies, helping with their cash management and credit needs.

8. Sofi

Sofi has been recognised to take a distinct approach, specialising in the credit side of personal finance and investments.

9. Upgrade

A US-focused lending platform in the banking network, Upgrade offers quite a balanced set of credit products to satisfy local demand.

10. Monzo

Monzo has shown to be a convenient saving tool and a digital wallet when it comes to everyday expenses. Its USPs not only feature interesting analytics and transaction speed but also forecasts.

To view the full list of Buy Now Pay Later (BNPL) Unicorns by Market Capitalisation, view our live ranking of the largest Fintech companies.

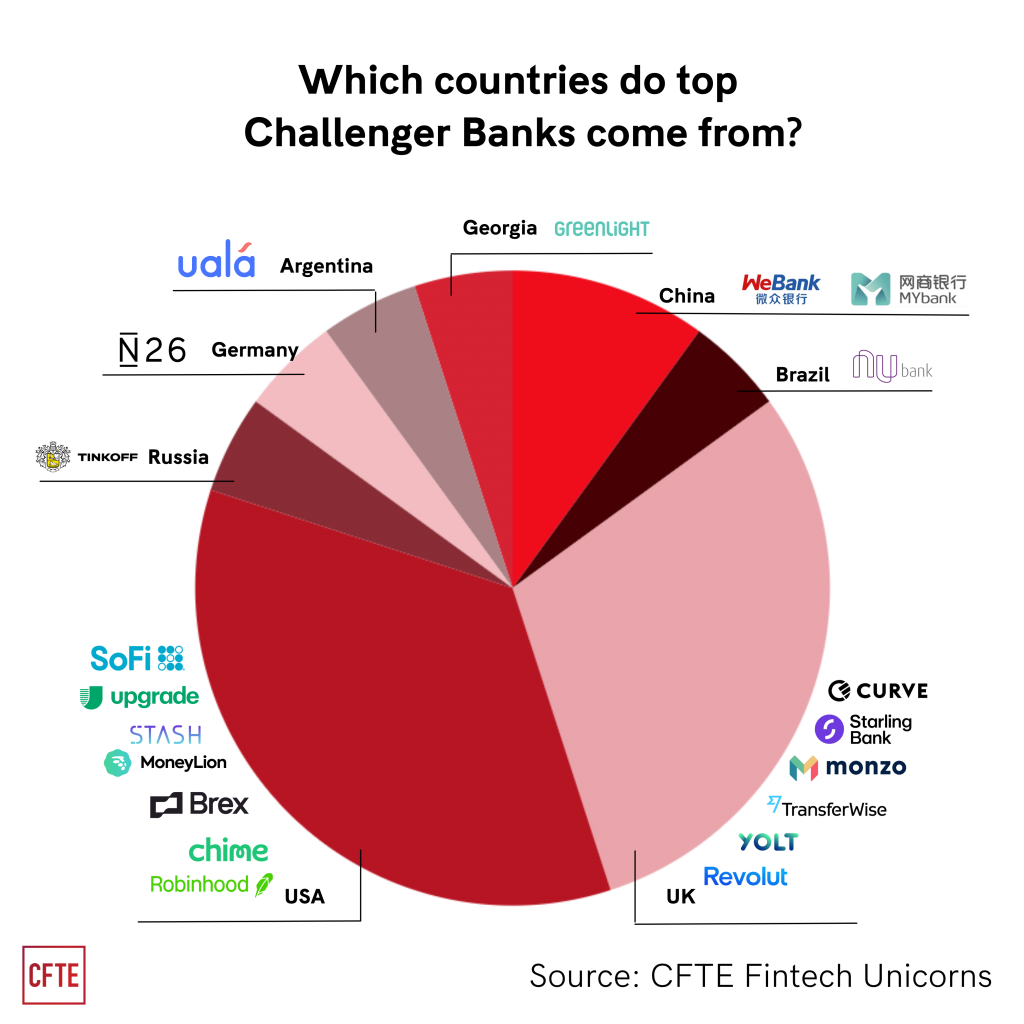

Which countries do the top Challenger Banks come from?

Among the top 20 Challenger banks in our dataset, 7 are from the USA, 6 from the UK, 2 from China, and 1-1 from Argentina, Brazil, Georgia, Germany, and Russia.

What are the trends in the Challenger Bank Sector for 2021-2022?

1.The topmost is not the US or the Uk but Brazil:

The most successful of the challenger banks is a Sao Paulo-based company called Nubank. While no one expects Nubank to dethrone the big five banks, they have forced them to improve their technology and close hundreds of physical locations as customer expectations alter.

2.Europe Leads with Good legislation:

The implementation of open banking, particularly the well-known PSD2, has facilitated the emergence and rapid growth of challenger banks. The United Kingdom, France, and Germany are among the countries leading the trend, with challenger banks such as Revolut leading the way.

3.The USA even after having the most number of Challenger banks lags behind:

The necessary regulatory changes unlike Europe are coming slowly in the USA.

What is the Future of Challenger Banks in the next 5 years?

1. Focused on freelancers and SMEs

Despite the fact that competition with banking institutions is one of the most significant obstacles for SME-focused banks, there is still plenty of room for expansion.

2. Cryptocurrency

Some may argue that cryptocurrencies are the polar opposite of the banking system due to their decentralization, but as more people become aware of cryptocurrencies, demand for a simple and user-friendly financial service will increase.

3.Hyper personalisation

For a long time, mainstream banks have offered some level of personalization in their services. Offering hyper-personalization in banking services will be a game-changer for digital banking in the next years.