Cash is going digital

Cash is king. But as the world is experiencing a digital evolution, the king is becoming more and more digitised. In a journal published in 2017 called ‘A Journey Towards a Cashless Society’, cashless transactions are reigning in countries where digital transformation is most embraced including Singapore, Netherlands, Sweden, Belgium and the United Kingdom.

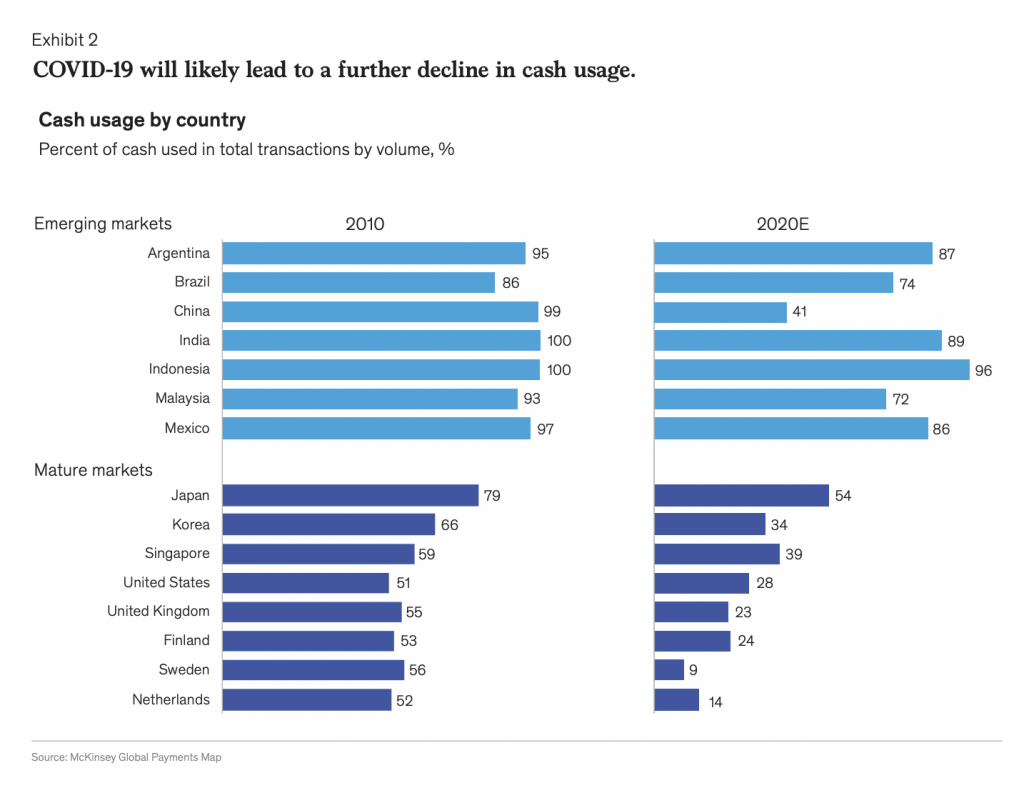

Whether you like it or not, a cashless society as a concept is becoming increasingly popular and inevitable. COVID-19 has also proven to be an accelerator to this global trend. With the rise of cryptocurrencies, stable coins, central bank digital currencies, and payment infrastructure fintechs, we are seeing a global economy setting itself up for the transfer of value through ‘ones and zeros’ instead of paper bills.

But why are we aiming towards a cashless society? What are the benefits of replacing paper currency with a digital equivalent on one’s smartphone or computer?

Why is the digitalisation of payments inevitable?

By digitalising transactions between parties, data is produced and represents the trail of the paper bill. Every time a party transfers funds from one bank account to another, a record of that transaction is made and stored in the data center of the bank/custodian. This transparency is what allows governments and institutions to trace the origin of the circulated money and detect any illegal practices behind such as trafficking, money laundering, fraud, or tax evasion.

Adding onto this benefit of keeping record, transactions are turned into data which can be used by data scientists at financial institutions or fintech startups to study customer behaviour and spending habits. The insights and information from this data analyses will then result in new innovations in financial services and products that can be better, faster, or cheaper for the end consumer. For instance, Kabbage is a $2.5 billion US startup that uses data lakes to provide AI-powered business loans for small businesses. Kreditech is also a fintech startup which relies on data lakes and machine learning models to offer the underbanked access to better credit than incumbent banks. In a digitally transforming world, financial transactions are critical for innovations in financial services.

It is also evident that cash management in physical form is much more costly and less secure than its digital counterpart. With the 256-bit advanced encryption standard (AES), it is extremely difficult for third parties to intercept and exploit consumer financial data. In addition, handling, storing and depositing physical cash is much more time consuming than transferring funds on a mobile app via a neobank. This is why consumers consider going cashless as time and effort are massively reduced, whilst security is greatly enhanced.

Implications of digitalisation of payments

However, as consumers embrace online transactions, this also means they are foregoing their anonymity in transactions. Since digital transactions are recorded and stored as data, if such data falls into the hands of cybercriminals or collusive organisations, consumer privacy and cash assets are at risk.

Inequality is also believed to be the side effect of a society going cashless. Data from the People’s Bank of China showed that in 2019, banks handled non-cash mobile payments of $49.27 trillion, an increase of more than 25% over the previous year. Surveys show roughly four out of every five payments in China are made through Tencent’s WeChat Pay or Alibaba’s Alipay. A reporter from CNBC visited Beijing and documented his experience trying to find vendors that would accept cash, only to realise that the city is inches towards going fully cashless. As most vendors reject receiving cash as payments, this limits transaction possibilities to those who can afford to have smart phones, internet connections, and digital acumen. This is where the question of income inequality comes in as the lower segment of the economy is segregated and further discriminated against for not having access to digital payments.

As societies progress towards digital forms of transferring information and value, it is seemingly inevitable that we are aiming towards a cashless society. The benefits of digital payments and storing of value are clear to the public as the essence of technology is to ensure living standards increase and customer satisfaction is prioritised. However, it is the larger social implications of digital payments that we are still discovering, one large scale financial scandal or malpractice at a time. It is important to acknowledge both sides of this financial evolution so that we as consumers can make the right decisions for our financial needs.

What do CFTE Experts think?

CFTE interviewed Ritesh Jain, Co-Founder of Infynit – a Fintech company that manages multiple customer credit cards all under one app with an innovative rewards management system embedded, about the possibility of digital wallets replacing cash. “I do not think that digital payments will completely replace cash… There are economies where cash is pretty much in circulation because of lack of internet, lack of access to financial services, lack of the digital payments infrastructure.” says Ritesh when asked whether digital payments/digital wallets replace cash. Despite this, there are economies and societies where cashless seems to be the dominant phenomenon. “The way I’m looking at it and reading around it, economies such as China, especially Finland, Sweden, and the UK, seems to be going cashless earlier than anybody else globally” says Ritesh Jain.